Disability Savings Plan

Build Financial Security with a Registered Disability Savings Plan

Get up to $90,000 in government Grants and Bonds + tax-free growth for your future

Why the RDSP

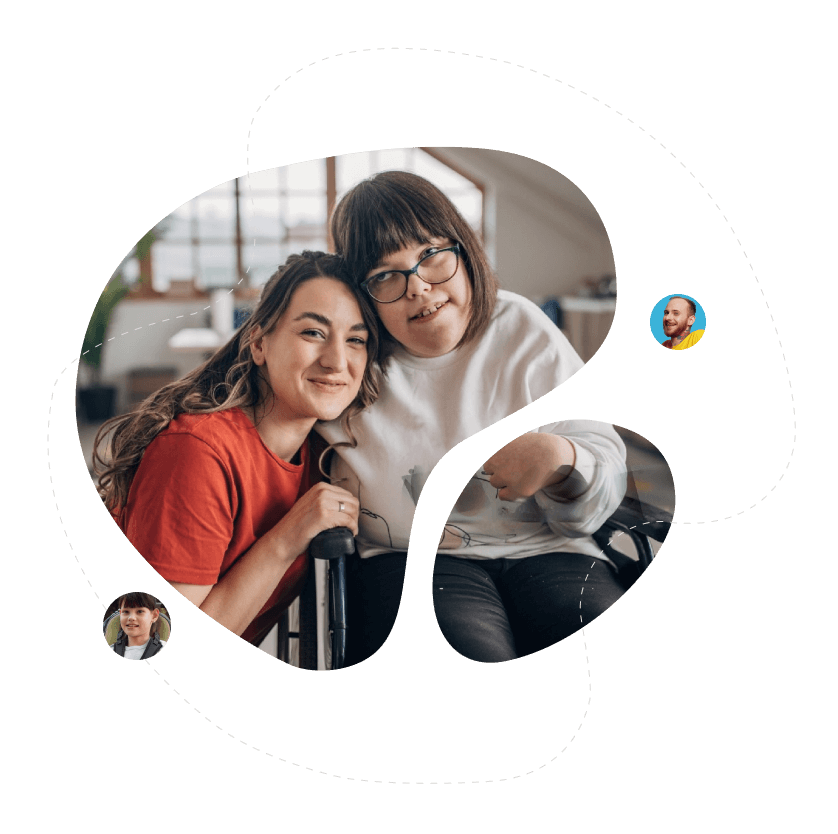

Empowering Futures: Why the RDSP Truly Matters

The RDSP empowers individuals with disabilities to build

long-term financial security. With government grants and bonds, it helps

families grow savings faster, ensuring future independence, stability, and

peace of mind for both beneficiaries and their loved ones.

Helping Canadians maximize their

RDSP benefits

Calculate Your Grant & Bond

Featured calculators

Grant Calculator

How much will the government match? Enter your annual contributions and family income for an instant estimate.

Bond Calculator

Do I qualify for free bonds? Check your family income and discover your eligibility in seconds.

Growth Projector

See your savings in 20 years. Enter your contribution details and visualize your RDSP’s growth over time.

Who Qualifies?

Eligibility Snapshot

Approved for DTC

The beneficiary must be certified by the Canada Revenue Agency (CRA) as eligible for the Disability Tax Credit (DTC). This foundational approval is mandatory to open and contribute to an RDSP.

Canadian Resident with Valid SIN

The individual named as the beneficiary must be a Canadian resident at the time the plan is opened and must possess a valid Social Insurance Number (SIN), as required by the government.

Under Age 60 When Opening

The RDSP must be established and opened before the beneficiary reaches the age of 60. Contributions are allowed up to the end of the year the beneficiary turns 59.

How we help

Getting started with a new plan

How to Open an RDSP

Step-by-Step Guide

Opening a Registered Disability Savings Plan (RDSP) is simple when you know the steps. Follow this guide to secure your loved one’s financial future with government grants and bonds.

Here’s how you can start:

- Confirm eligibility for the RDSP

- Gather SIN and disability documentation

- Choose your financial institution

- Open the RDSP account together

- Apply for grants and bonds

- Monitor your RDSP growth regularly

Why Choose the

RDSP Plan

The Registered Disability Savings Plan (RDSP) helps Canadians with disabilities secure long-term financial stability through government grants and bonds.

With the RDSP, you can:

- Grow your savings with government contributions

- Receive up to $70,000 in lifetime grants

- Receive up to $20,000 in bonds even without contributions

- Build long-term financial independence

- Ensure your loved one’s secure future

- Access funds for education, housing, or care needs

our testimonial

why clients love us

Emilio

Client

5.0

"Caring Hands provided exceptional support for my son's RDSP journey. Their expertise helped us navigate easily and make the most of government grants."

Irfan Parvez

Parent

5.0

"Thanks to their clear guidance, setting up my daughter’s RDSP was simple. The team explained every detail and helped us maximize our savings."

Yolisawa Mlambo

Beneficiary

5.0

"My RDSP has given me peace of mind about my future. Their personalized approach made a big difference in planning my finances."

Harpreet

Parent

5.0

"Their RDSP knowledge is outstanding. They make the process stress-free for families and ensure every eligible grant is claimed efficiently."

Dembe

Client

5.0

"I appreciate how patient and helpful the team was. They helped me understand every step and showed how the RDSP can secure my Brother’s future."

Geeta Vij

Parent

5.0

"They truly care about families. Their RDSP advice helped us plan a secure, confident future for our son with disabilities."